工程保險

承包商全險

保障工地免受意外、財產損失及第三方責任影響 — 將工程物料損毀、第三者責任及勞保整合於一張保單,工程更安心。

報價同日簽發 Certificate of Insurance。

比較各家保險公司議價。

深受香港大型工程信賴

由港鐵基建工程、醫管局裝修,到莎莎零售門市、第一太平戴維斯管理物業及西九文化區項目 — 承建商均選用 LSC 工程全險。

上午遞交資料 — 即日簽發保險證書,工程準時開工,避免延誤及違約罰款。

承包商全險(CAR)

工程保險(又稱裝修保險)為裝修及建築工程提供保障,承保期間突發的金錢損失或賠償責任,將工程物料損毀、第三者責任及僱員補償整合於一張保單。

無論是承接單一裝修工程,還是同時管理多個工地的承建商,CAR 保單均可按合約條款及工地風險度身配置 — 讓意外、天氣及第三方索償不會影響工程進度。

我們承保的工程類別

由小型店鋪裝修到專業設備安裝 — 以下是我們最常處理的工程類型。

工程保險的保障範圍

工程保險將工地必備的三大保障整合於同一份保單。

以全險形式保障工程及物料免受火災、盜竊、水浸及其他工地意外造成的損失。

保障業務因工程運作對第三者造成的身體傷害、財物損失或人身傷害,包括法律費用、和解金及醫療費用。

香港法例規定所有僱主必須投保,覆蓋工人於工地的醫療、傷殘賠償及收入損失,包括職業病。

報價工程保險所需資料

提供以下資料,我們通常可即日回覆報價。若有缺漏,歡迎 WhatsApp 我們協助整理。

- 工程合約報價單

- 工程額(HK$)

- 工程承辦商(英文)

- 管理公司(英文)

- 僱主(英文)

- 工程地址(英文)

- 工程期 + 補修期

- 是否使用棚架/吊船/工作台?

- 室外工程是否超過 20% 工程額?

- 保障範圍:物料損失、第三者責任(買幾多?)、勞保

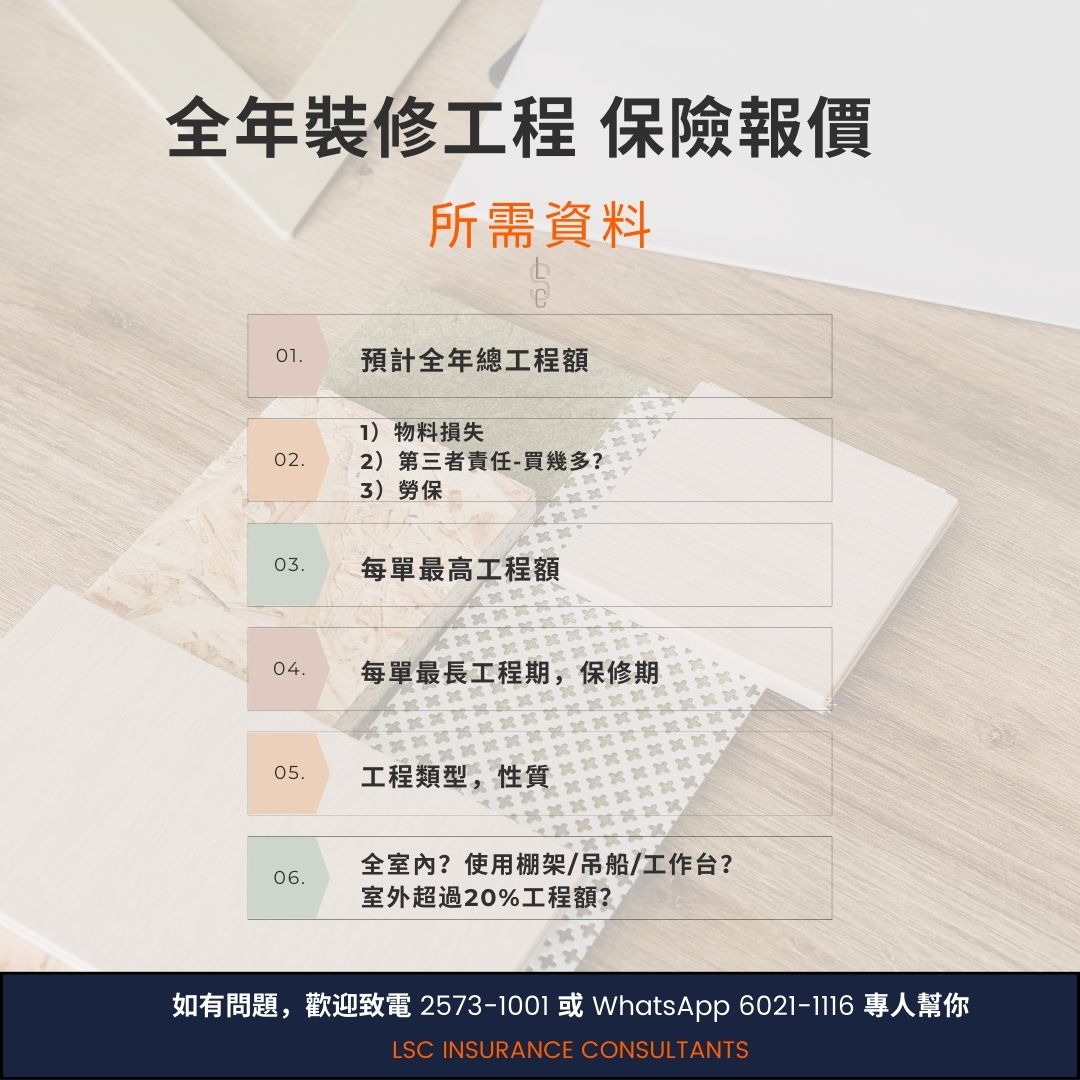

全年裝修工程保險(按工程額)報價所需資料

如選用全年保單按工程額計算,請提供以下資料,方便我們為您安排合適的限額及保險公司。

- 預計全年總工程額

- 所需保障:物料損失、第三者責任(買幾多?)、勞保

- 每單最高工程額

- 每單最長工程期、保修期

- 工程類型及性質

- 全室內?使用棚架/吊船/工作平台?室外超過 20% 工程額?

勞保:MPF 人工計算 vs 工程額計算

承辦商可以兩種方式投保勞保 — 視乎您實際的工程運作及二判安排選擇最合適的計算基礎。

一般勞工保險

- 通常只保受保公司之僱員

- 用一年人工人數去買

- 通常用 MPF 來核實

- 不需要訂立限額

- 通常只保受保公司

適合:自家僱員、文職、人工固定的公司。

工程勞工保險

- 可以保埋二判及所有承判商

- 用預計全年總工程額去買

- Year-end Declaration & Premium Adjustment — 多除少補

- 需要訂立每單最高工程額、最長工程期、保修期;如有項目超過限額,需另買一次性保險

- 可以落埋你大判 — 客人做受保人

適合:有二判、人手浮動、同時開多個工地的承辦商。

不確定該用哪種基礎?我們會根據您的工程量、二判安排及大判要求,建議最合適的保單結構及保險公司。

工程保險 8 大注意事項

提交完整工程報價

提供整份工程報價以便評估風險。如使用棚架、密閉空間、工作平台、特殊機械或吊船須事先告知。

了解保障範圍

細閱報價單上的保障、限制及不保事項,有疑問請先聯絡我們澄清。

工程開始前投保

保單須於工程動工前購買。保單期須與實際施工期一致,如工程未完成,須在到期日前通知保險公司。

工程變更須通報

工程總額或性質有重大變更須通知保險公司,否則保險公司有權拒賠。

留意墊底費

墊底費越高保費越低,但出險時自付金額越大。投保前須多比較。

加入業主為附加被保人

業主可要求裝修公司將業主及管理公司列為附加被保人,較單獨投保更具成本效益。

核實裝修公司的保單

業主應核實承建商的勞保及第三者保險 — 保險公司名稱、有效期、投保人數及工作性質均須核對。

棚架及不保事項

室內裝修保單通常不包括棚架架設、拆卸及外牆工程。請確認工程性質條款與實際情況相符。

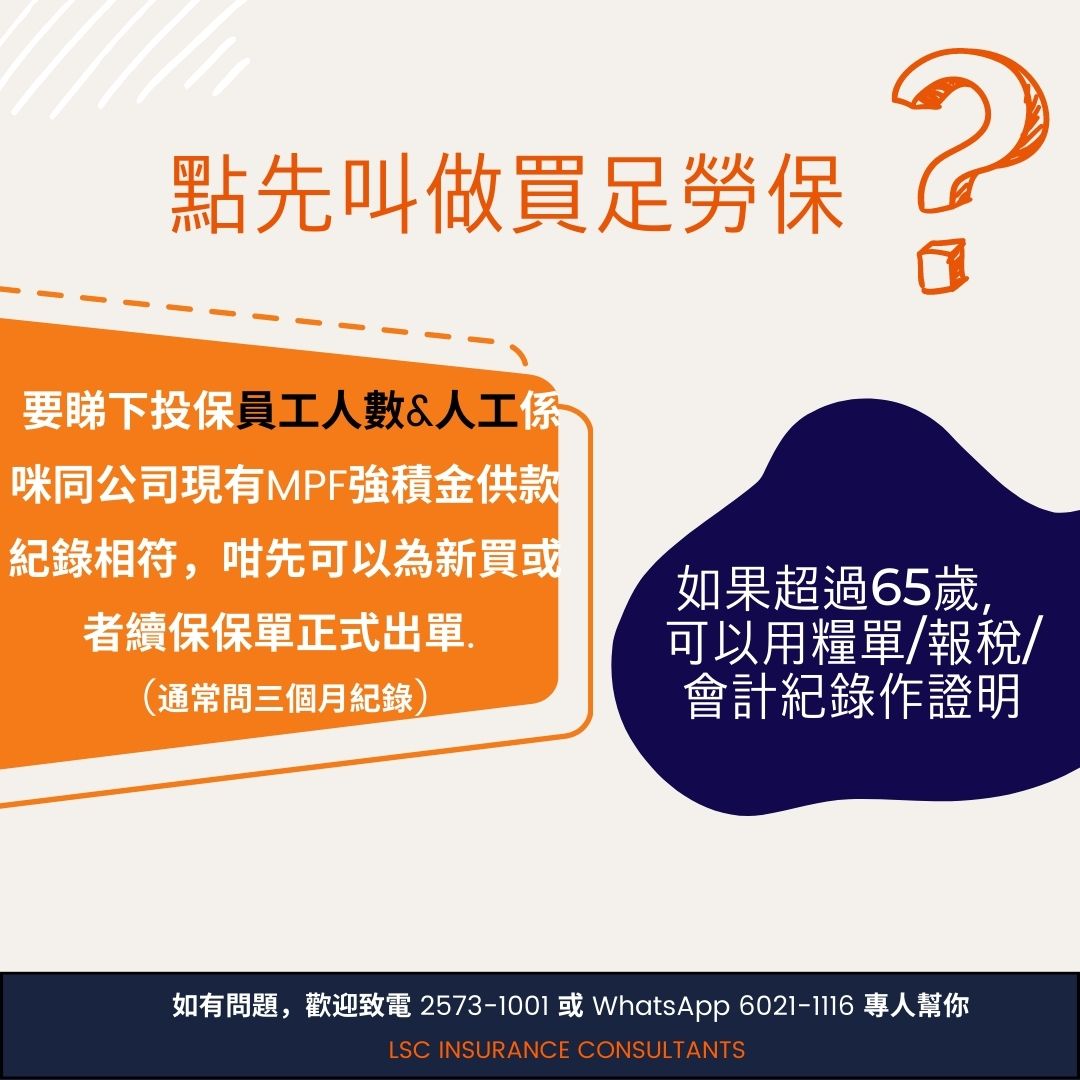

點先叫做買足勞保?

保險公司會核對投保員工人數及人工是否與公司MPF強積金供款紀錄相符;如有差異,索償時可能被打折甚至拒賠。以下是香港保險公司新買或續保時通常採用的準則。

人數及人工須與MPF紀錄相符

保險公司新買或續保前,通常會要求提交最近3個月的MPF強積金供款紀錄,核對員工名單、人數及人工是否一致。

65歲以上員工 — 可用其他文件證明

65歲以上員工豁免供強積金,可以用糧單、報稅表 (IR56) 或會計紀錄作為人工證明。

漏報/少報的風險

若索償時實際人工高於投保時申報,保險公司可按比例賠償(average condition),甚至以未如實申報為由拒賠。

- 申報總薪金(gross),而非實發薪金

- 包括花紅、佣金、津貼及加班費

- 增聘人手或加薪時要中途通知保險公司更新

勞保 Warranty — 僱主必讀

保險公司通常會根據你的行業性質,在勞保保單上加入相關 Warranty 以控制風險。如果僱員實際工作違反 Warranty,有機會令保單無效,影響索償。

甚麼是 Warranty?

是特定條款,限制你的僱員不可以做某些工作。如果違反,有機會令保單無效,影響索償。

投保前必須核對

請留意保單會否落咗邊條 Warranty 不適用於你公司僱員實際工作需要。

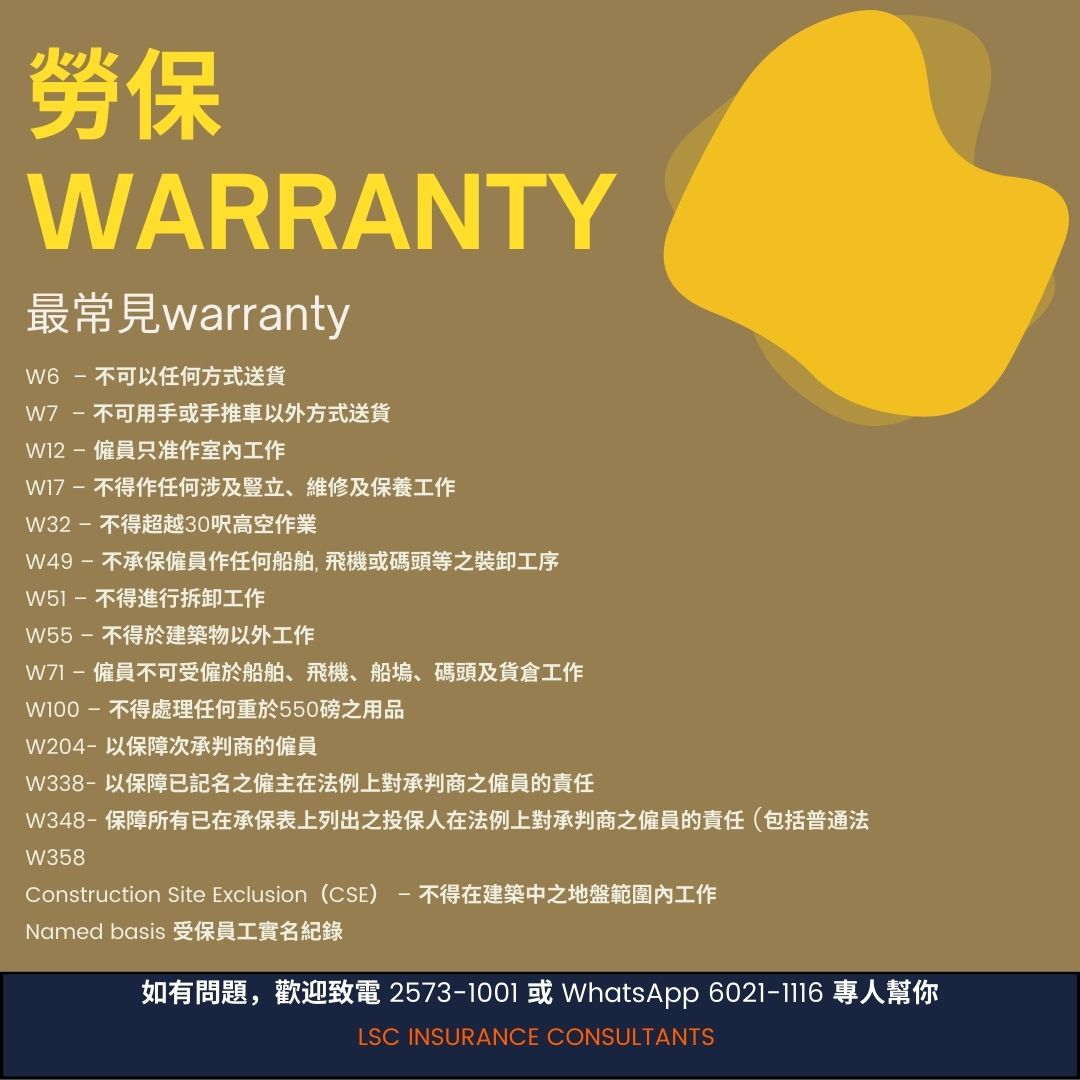

最常見勞保 Warranty

僅供參考,最終以保單為準。

- W6不可以任何方式送貨

- W7不可用手或手推車以外方式送貨

- W12僱員只准作室內工作

- W17不得作任何涉及豎立、維修及保養工作

- W32不得超越 30 呎高空作業

- W49不承保僱員作任何船舶、飛機或碼頭等之裝卸工序

- W51不得進行拆卸工作

- W55不得於建築物以外工作

- W71僱員不可受僱於船舶、飛機、船塢、碼頭及貨倉工作

- W100不得處理任何重於 550 磅之用品

- W204以保障次承判商的僱員

- W338以保障已記名之僱主在法例上對承判商之僱員的責任

- W348保障所有已在承保表上列出之投保人在法例上對承判商之僱員的責任(包括普通法)

- CSEConstruction Site Exclusion — 不得在建築中之地盤範圍內工作

- Named basis受保員工實名紀錄

不確定保單上的 Warranty 是否切合你的實際運作?將保單發給我們,我們會免費檢閱並標示有機會影響索償的條款。

全面保障,客戶至上。

與領先保險公司建立深厚關係,四十年經驗讓我們深諳承保偏好,談判力強。

深入了解您的營運及工程節奏,持續提供支援。

我們只為您工作,挑戰不公平的不保事項,爭取更佳條款。

事故發生即時行動,清晰指引文件要求。

由我們對接保險公司及理賠員,讓您專注工程。

持牌經紀及索償專家,具備工程理賠豐富經驗。

全面分析,找出潛在工地風險。

審核第三方合約要求,確保保單符合總承包商及場地的條款。

目標較現有保費節省 15%。

LSC vs 代理 vs 保險公司

| LSC 保險經紀 | 保險代理 | 保險公司 | |

|---|---|---|---|

| 服務對象 | 你(以客為先) | 代表的保險公司 | 股東 |

| 保險公司選擇 | 30+ 保險公司 | 1–4 家合作 | 只賣自家產品 |

| 產品範圍 | 全面 | 有限 | 細分及受限 |

| 客製化 | 度身企業方案 | 個人產品 | 標準套裝 |

| 風險建議 | 主動專業 | 基本 | 銷售為主 |

| 索償支援 | 全程跟進 | 有限 | 熱線為主 |

| 成本效益 | 議價優惠 | 選擇有限 | 固定價格 |

| 合規協助 | 有(合約及《條例》) | 極少 | 無 |

常見問題

單次工程保單與全年保單有甚麼分別?+

單次保單適合規模較小或不定期的工程,沒有年度最低保費;全年保單則為承接多項工程的公司提供穩定保費及簡化的行政處理。

工程保險是否包括拆卸主力牆或僭建物?+

一般情況下不會承保,需額外加保並列明條款。

如果工程超出保單有效期會怎樣?+

必須在保單到期前通知保險公司,逾期通知保險公司有權拒絕延期。