Employees' Compensation

Labour Insurance

Protection that supports your team — covering work-related injuries, illnesses and employer liability, so your business and workforce stay secure every day.

Issued the same business day.

Negotiated rates across insurers.

Submit your documents in the morning — get your CoI in time to meet contract, venue or licensing requirements today.

Employees' Compensation Insurance (EC)

Employees' compensation protects employees who suffer accidents at work or contract occupational diseases specified in the Employees' Compensation Ordinance, and provides compensation in accordance with Hong Kong law. All employers must insure each employee to ensure their basic rights and interests.

According to Section 40 of the Employees' Compensation Ordinance, all employers must take out EC insurance to assume legal liability. Employees may not be employed to perform any work — regardless of contract period, working hours, full-time or part-time status — without cover.

Industries we cover

Some examples of sectors where our EC solutions are most often deployed.

Compensation for work-related injuries

Five categories of compensation employers must pay under the HK ECO — all covered when properly insured.

If an employee permanently loses work capacity — fully or partially — due to a work injury, the employer must pay the corresponding compensation as assessed under the Ordinance.

When a registered doctor or assessment board certifies absence from work, the employer pays 75% of the difference between pre-injury and during-leave monthly earnings.

Employers cover all medical costs arising from the work injury — consultation fees, hospitalisation, medication and treatment supplies.

If an employee dies from a work injury, the employer pays compensation to the family — including funeral and outstanding medical expenses.

Pain & suffering, loss of enjoyment of life, loss of income and future earning capacity — plus special items such as medical, transport and attorney fees.

6 things to check when purchasing EC

Name of policyholder

Company name correct and consistent with employment and MPF contracts.

Nature of business

Business nature on quotation matches what you actually do.

Number of employees

Insured headcount must equal total staff — insurers don't accept sharing.

Annual salary

Quote uses expected salary for the coming year; refunded or topped up at year-end.

Work location

Long-term work locations of employees are clearly stated.

Employee position

Roles and nature of work clearly described — manual, aerial, machinery — and any exclusions noted.

Protecting teams across industries

From retail and F&B to professional services — employers of every size rely on LSC for statutory EC cover.

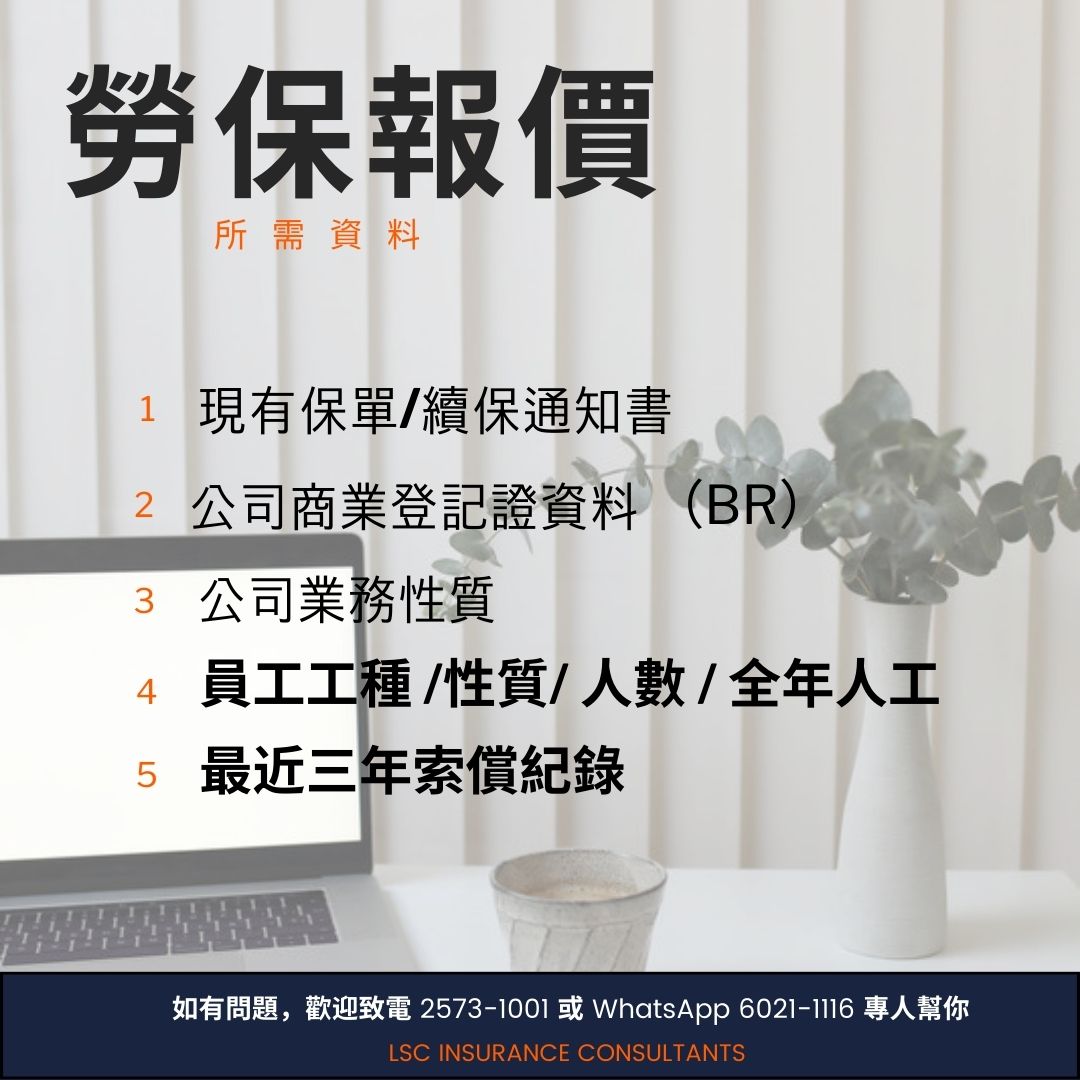

Information we need to quote EC insurance

Send us the following and we'll usually come back to you the same day.

- Current policy schedule / renewal notice

- Business Registration (BR) details

- Nature of business

- Staff roles / duties / headcount / total annual wages

- Last 3 years' claims record

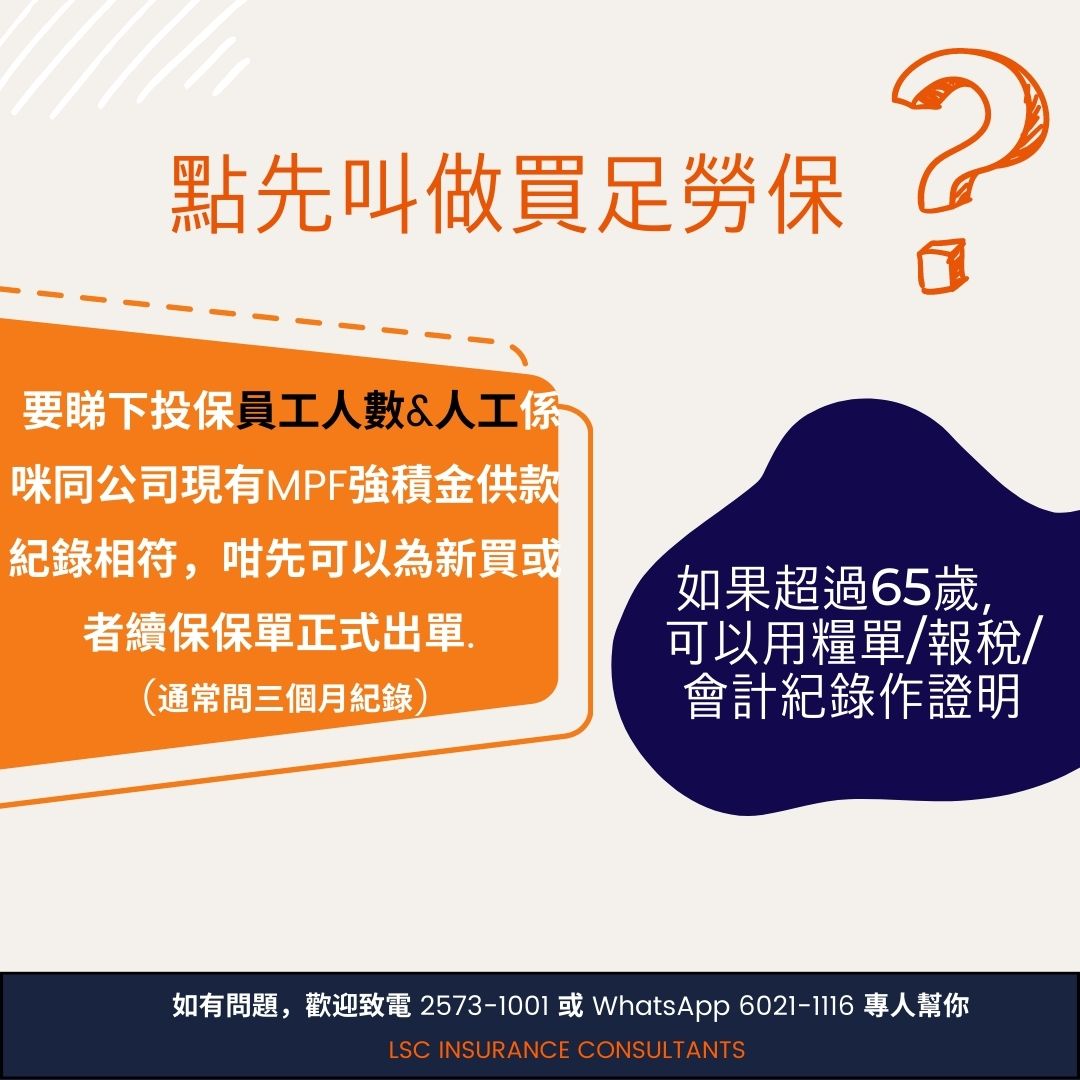

What does it mean to buy enough EC cover?

Insurers want to see your declared headcount and wages match your actual MPF contribution records — otherwise claims can be reduced or repudiated. Here's the rule of thumb HK insurers apply when issuing or renewing an EC policy.

Headcount & wages must match MPF records

Insurers usually request the latest 3 months of MPF contribution records before issuing a new or renewal EC policy. The names, headcount and wages on the proposal should match.

Staff aged over 65 — alternative proof accepted

Employees over 65 are exempt from MPF. For these workers you can provide salary slips, tax returns (IR56) or accounting records as proof of wages.

Under-declaring is risky

If actual wages exceed the declared figure at claim time, the insurer may apply average condition — paying only the proportion that was actually insured. Worst case: the claim is rejected for material non-disclosure.

- Declare gross annual wages, not net pay

- Include bonuses, commissions, allowances and overtime

- Update mid-term when you hire or your wage bill grows

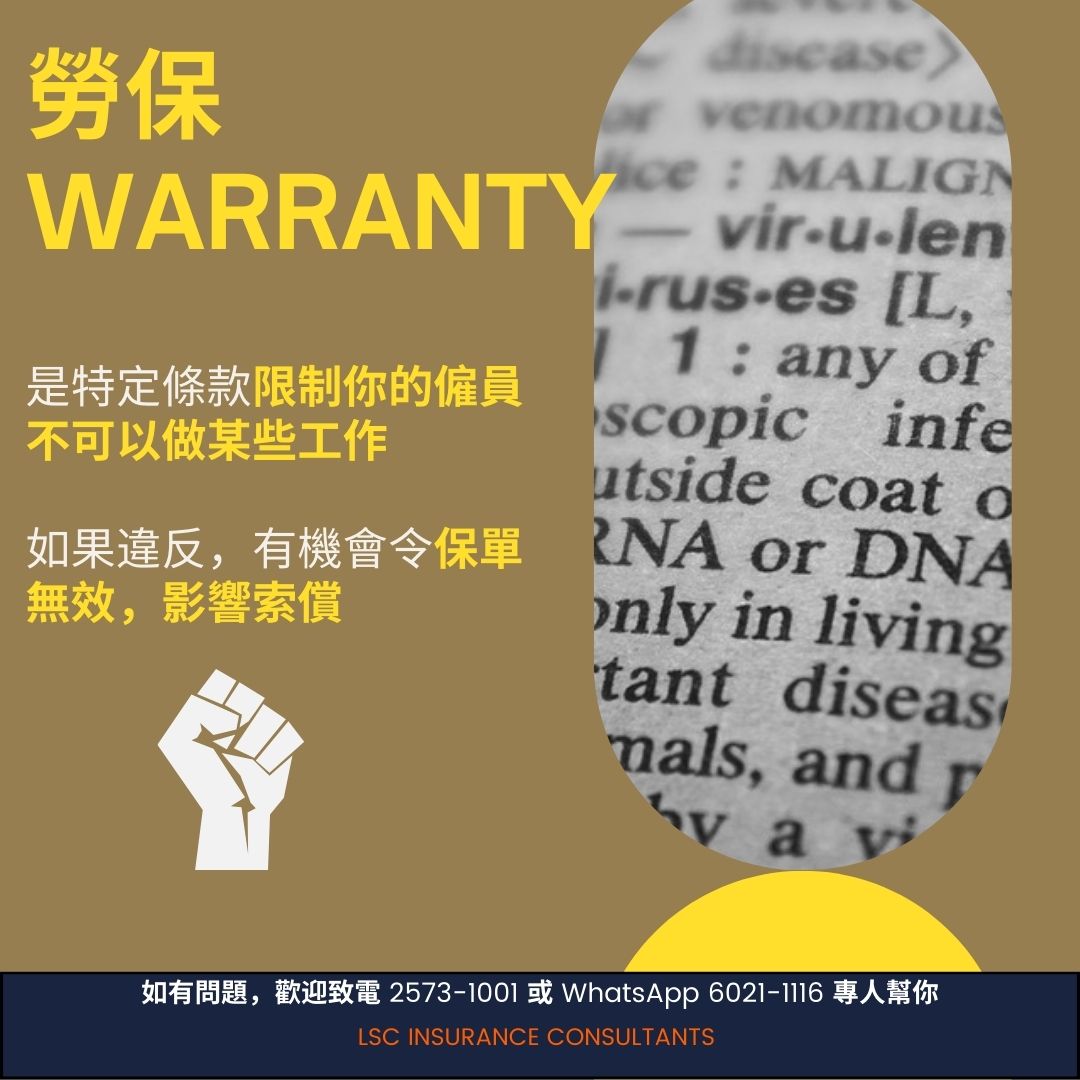

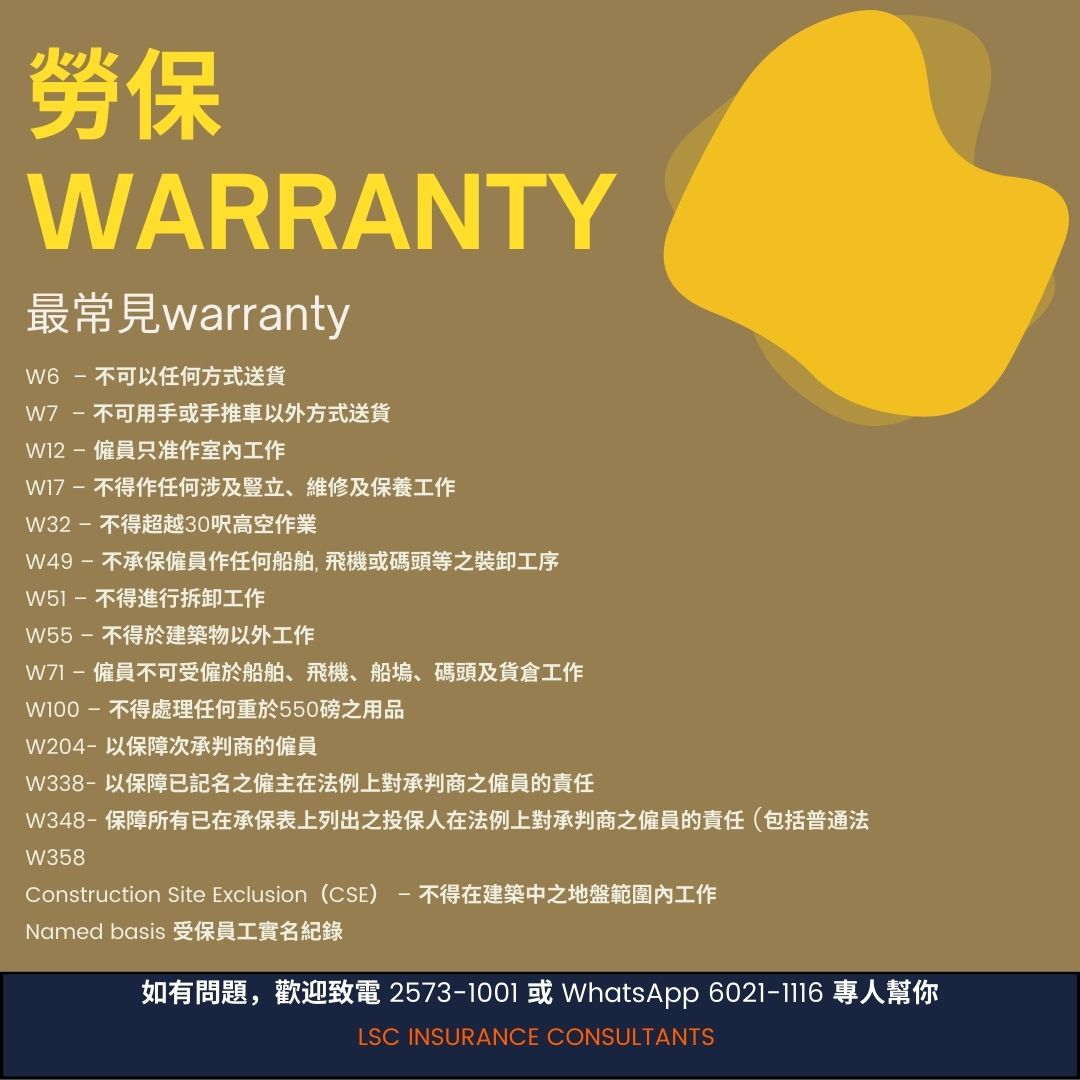

EC Warranty — what every employer should know

Insurers attach Warranties to your EC policy to control risk based on your industry. If your employees' actual work falls outside a Warranty, your policy may be voided and a claim refused.

What is a Warranty?

A specific policy clause that restricts what your employees are allowed to do. Breach a Warranty and the insurer may void the policy and refuse to pay a claim.

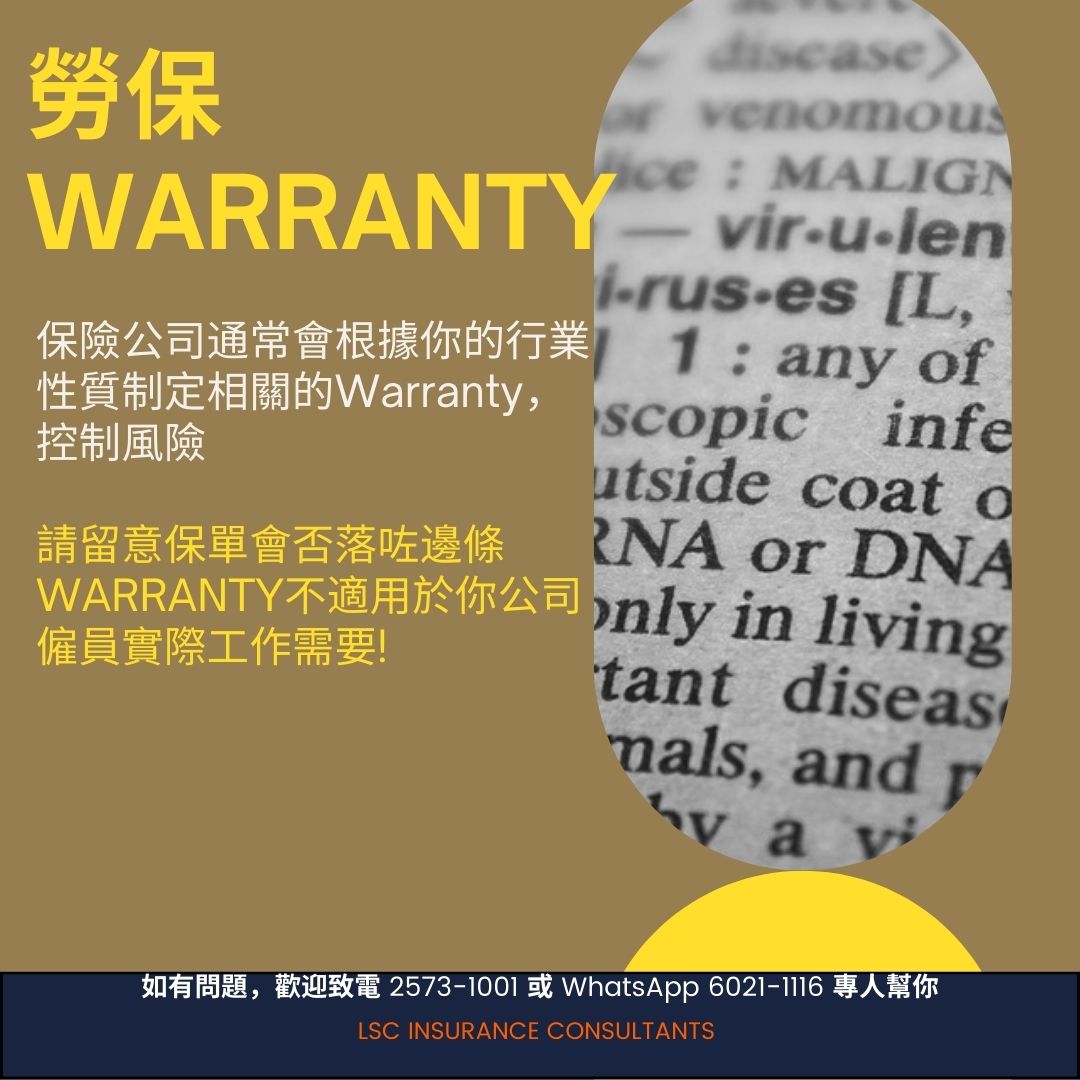

Always check before you bind

Review which Warranties the insurer attached and make sure none of them conflict with what your team actually does on the job.

Most common EC Warranties

For reference only — exact wording follows the policy schedule.

- W6No delivery of goods by any means

- W7No delivery other than by hand or hand-trolley

- W12Employees restricted to indoor work only

- W17No erection, repair or maintenance work

- W32No work above 30 feet (height)

- W49Excludes loading/unloading on vessels, aircraft or docks

- W51No demolition work

- W55No work outside the building

- W71Employees not employed on vessels, aircraft, docks, piers or warehouses

- W100No handling of items over 550 lbs

- W204Extension to cover sub-contractors' employees

- W338Covers the named principal's legal liability for sub-contractors' employees

- W348Covers all insured listed on schedule for legal liability to sub-contractors' employees (incl. common law)

- CSEConstruction Site Exclusion — no work within a construction site

- Named basisCover applies on a named-employee basis only

Not sure if a Warranty fits your operations? Send us your policy — we'll review it and flag any clause that may conflict with your real work.

Which workers must be covered by EC?

Hong Kong's Employees' Compensation Ordinance covers anyone with an employer–employee relationship — regardless of hours, location or contract type. Self-employed individuals and independent sub-contractors fall outside.

Must be covered

- Part-time employees

- Salaried directors / bosses (of a Limited Co.)

- Overseas employees on company assignment

- Summer interns / trainees

- Part-time domestic helpers

Not required

- Sub-contractors (with their own staff)

- Self-employed persons (no employer)

Sub-contractors should hold their own EC policy for their own staff.

I'm the boss — do I need EC for myself?

It depends on your company's legal structure. The trick: a Limited Company is a separate legal entity, so even the boss is technically its 'employee'.

The company is the employer. Both the salaried director/boss and all salaried staff are employees of the company.

- Salaried director / boss Required

- Salaried employees Required

The boss IS the business — legally self-employed, not an employee. EC is only required for the people they hire.

- Boss = self-employed Not required

- Salaried employees Required

Already insured? Why get an alternative quote from us

Renewing on auto-pilot is the easiest way to overpay or stay under-covered. A 5-minute alternative quote gives you three concrete wins.

Review your existing policy

We read your current schedule and flag warranties, sums insured or exclusions that no longer fit your operations — before they hurt a claim.

Reset to a clean-claim rate

Quotes typically only consider the last 3 years of claims history. If a past incident is older than that, you're effectively a clean risk — and that often unlocks a lower premium.

Get a commercial-line specialist

If your current agent mainly handles life or personal insurance, EC and commercial claims can fall outside their day-to-day. A commercial specialist follows up your claim end-to-end.

Comprehensive protection. Unmatched advocacy.

Deep relationships with leading insurers and four decades of experience — unmatched insight and bargaining power.

We learn your operations intimately and support you as needs evolve.

We work for you, not the insurers — challenging unfair exclusions and securing better terms.

Swift action with clear documentation guidance — claims process as fast as possible.

We handle insurer communication and follow up with adjusters so you focus on business.

Licensed brokers and claims specialists with decades of combined experience.

Thorough analysis to identify vulnerabilities standard insurers overlook.

Plain-English explanations tailored to your business and risk appetite.

We target a 15% premium reduction vs. existing cover, leveraging local insurer relationships.

LSC vs Agent vs Insurer

| LSC (Broker) | Agent | Insurer | |

|---|---|---|---|

| Works for | You (client-focused) | The insurer | Shareholders |

| Choice of insurer | 30+ insurers | 1–4 partners | Own products only |

| Product scope | Comprehensive | Limited | Niche & restricted |

| Customisation | Tailored corporate | Personal life | Standard package |

| Risk advice | Proactive expertise | Basic guidance | Sales-driven |

| Claim support | End-to-end advocacy | Limited | Hotline only |

| Cost efficiency | Negotiated rates | Limited options | Fixed pricing |

| Compliance help | Yes (HK ECO, S.88) | Minimal | None |

Common questions

Is EC insurance legally required in Hong Kong?+

Yes. Under Section 40 of the Employees' Compensation Ordinance (Cap. 282), every employer must insure each employee — full-time, part-time, casual or contract — regardless of working hours or wage level. Non-compliance carries a fine of up to HK$100,000 and imprisonment of up to 2 years.

What factors determine my EC premium?+

Premiums are driven primarily by trade classification (risk grade) and total annual wages, then adjusted for claims history, headcount, job duties (e.g. working at height, machinery, driving), and safety record. High-risk trades such as construction attract higher rates and may require facility-scheme placement.

How can I lower my EC premium?+

Declare accurate wages and duties, maintain a clean claims record, implement documented OSH measures, and consider bundling with a package policy. Working with a broker that holds preferred terms with 30+ insurers typically secures rates 10–20% below direct quotes.

Is there an age limit for insured employees?+

There is no statutory age limit under the Ordinance. However, individual insurers may load the premium or impose conditions for employees above a certain age depending on the trade.

What is an unnamed (no-name) EC policy?+

An unnamed policy covers employees by headcount and job category rather than listing each worker by name. It suits businesses with frequent staff turnover — such as F&B, retail and event operations — and simplifies day-to-day administration.

Can I insure only one part-time employee if staff rotate often?+

Only under a strict 'one-for-one' replacement (Employee A leaves, Employee B takes the same role). If A, B and C work concurrently — even on rotating shifts — all must be insured. Coverage must match actual headcount at any given time.

What counts as a work injury under the Ordinance?+

Any accident arising out of and in the course of employment, including injuries sustained while travelling on employer-arranged transport, commuting during Typhoon Signal 8 or Black Rainstorm warnings, or while performing work duties outside Hong Kong under a HK employment contract.

When is the employer NOT liable for compensation?+

Liability is excluded if the injury is self-inflicted, caused by the employee's serious and wilful misconduct, attributable to intoxication or drug addiction (and not resulting in death or serious permanent incapacity), or if the employee made a false declaration about pre-existing injury.

What if actual wages differ from the estimate at policy inception?+

Premiums are adjusted at policy expiry on a 'refund-excess / pay-shortfall' basis once actual payroll is declared. Under-declaration can also reduce claim payouts proportionally.

How quickly can LSC issue a Certificate of Insurance?+

Standard trades receive a same-day quotation and Certificate upon confirmation. High-risk or facility-scheme cases typically take 1–3 working days.

10% off for new customers

Instant quote and follow-up. WhatsApp our team — pre-filled message gets you started in seconds.

WhatsApp us now