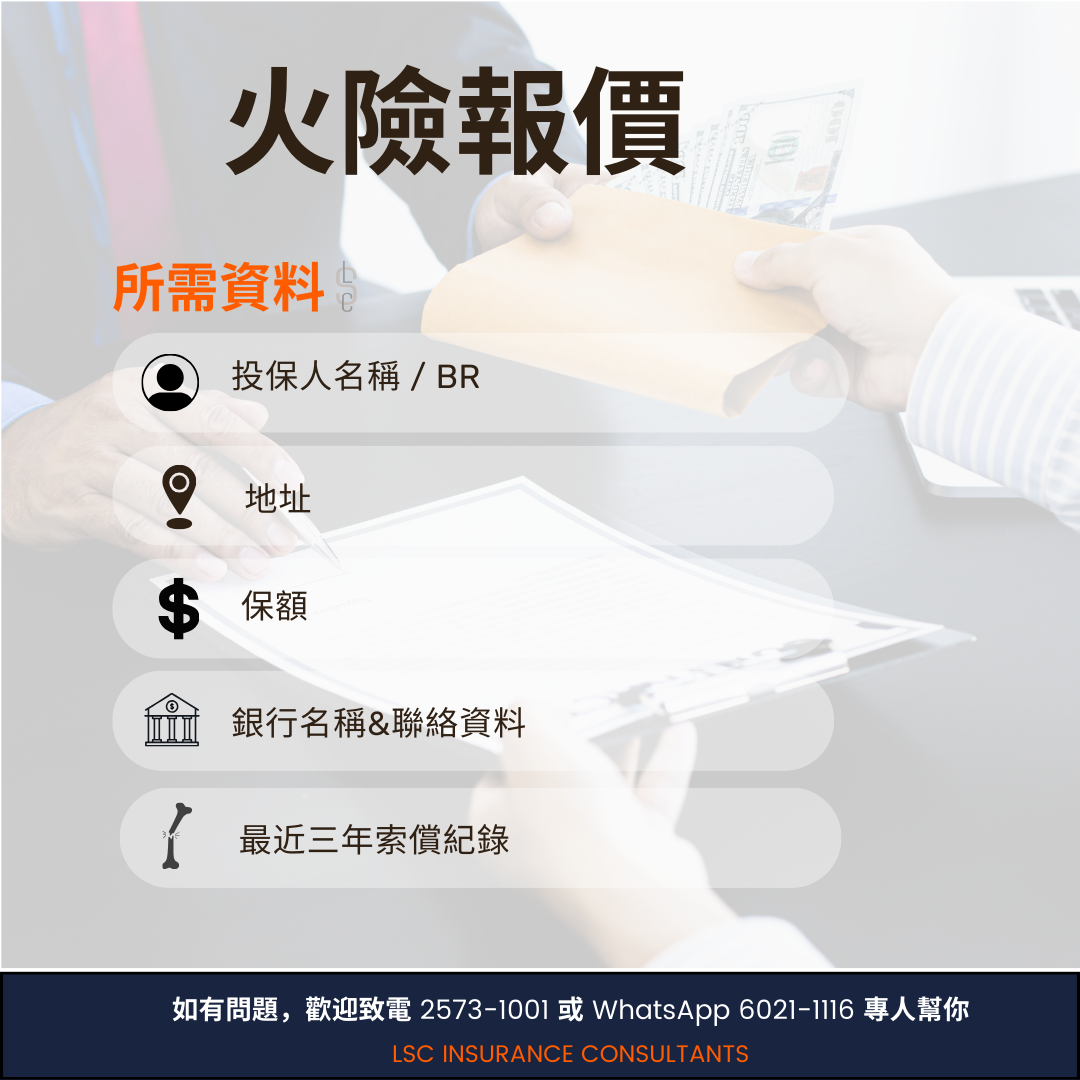

火 險

為香港住宅、商業及工業物業提供樓宇結構保障。保費率低至 0.03%,並由我們免費代送保單到您的銀行。

- 保費率低至 0.03%

- 免費代送銀行

- 即日簽發保險證明書

- 比較 30+ 家香港保險公司

即使物業已供斷,火險仍然不可或缺。

不少香港業主以為火險只是供樓期間銀行的要求,一旦供斷便讓保單失效,結果樓宇結構完全沒有保障。

2025 年大埔宏福苑火災正是慘痛的提醒。不少受影響的住戶並沒有為自己單位的樓宇結構投保火險,如今須自行承擔重建及修復費用,每戶可能涉及數百萬港元的財務損失。

火險在香港屬於最便宜的保單之一,通常每年只需數百港元,但若未投保,一場意外便可能改寫一個家庭的財務未來。

宏福苑火災(大埔,2025)

- 嚴重的高層火災,多幢樓宇結構受到廣泛損毀。

- 不少住戶在供斷物業後,便沒有續保火險。

- 未投保的業主須自費承擔重建、清拆及修復費用。

- 一張每年不足港幣 1,000 元的火險,可能已避免數百萬元的損失。

我們承保的物業類型

住宅、商業、工業及貨倉 — 我們承保香港各類常見物業的火險。

符合香港銀行要求的火險核心保障

以「重建費用」為投保額基準,加註按揭權益,並可附加香港銀行常要求的延伸保障。

火災、雷擊及爆炸

保障樓宇結構因火災、雷擊及爆炸引致的損失,是每張按揭火險的核心保障。

以「重建費用」投保

投保額以物業重建成本(建材、工資、清拆及專業費用)為基準,確保全損時能完整重建。

按揭權益加註

將銀行或財務公司加註為按揭權益人 — 符合香港所有貸款機構在成交時的標準要求。

可選附加保障

可加保颱風、水浸、爆水管、暴動及罷工、惡意損毀及碰撞等附加保障 — 部分樓宇類型銀行會指定要求。

低保費,並由我們代您處理銀行事宜。

免費代送保單到銀行

我們將正本保單及保險證明書直接遞交您的按揭銀行或財務公司 — 完全免費,確保成交不會延誤。

一次配對銀行要求

將銀行要求函交給我們,我們會安排投保額、按揭條款、承保風險及特別加註,令保單一次提交即獲接納。

保費率低至 0.03%

憑藉比較 30+ 家香港保險公司及 40 年承保關係,我們為合資格住宅及商業物業爭取低至投保額 0.03% 的保費率。

投保前留意保單內的建築類別,否則會影響賠償

尤其是有貨倉或工業大廈的公司。火險保單會按外牆及屋頂結構將建築分為 Class I、II、III,保單上類別錯誤可能令索償受影響甚至被拒。

全堅固結構

外牆及屋頂全部以混凝土、磚或石建造。

半堅固結構

屋頂為石棉板或鐵皮,配合密封式金屬/混凝土/磚/石外牆。

次級結構

非 Class I 或 II 之結構。露天儲存一律視為 Class III。

投保前請與經紀核對建築類別。在香港,建築類別申報錯誤是火險索償受影響的最常見原因之一。

火險 vs 家居保險 — 究竟有甚麼分別?

兩者名字相近,但保障範圍完全不同。大部分香港家庭其實兩者都需要:火險保樓宇結構,家居保險保室內財物及對第三者的責任。

| 項目 | 火險 | 家居保險 |

|---|---|---|

| 保障對象 | 只保樓宇結構(牆身、地板、天花、固定裝置) | 室內財物 — 傢俬、電器、貴重物品、衣物 |

| 誰會要求 | 按揭銀行 — 供樓期內強制要求 | 非強制 — 但每個家庭都建議投保 |

| 第三者責任 | 不包 | 包 — 例如漏水至下層、訪客在屋內受傷 |

| 颱風 / 水浸 / 爆水管 | 可加保(只保結構) | 通常包括(保財物) |

| 盜竊 / 爆竊 | 不保 | 受保(須有強行進入證據) |

| 每年保費(參考) | 由數百港元起 — 保費率低至投保額 0.03% | 約港幣 500 – 2,000 元,視乎財物價值 |

簡單記法:火險滿足銀行要求並重建樓宇外殼;家居保險則賠償室內財物,並承擔您對他人造成損失的責任。

火險不會保障的事項

火險的保障範圍刻意精簡,目的只是滿足銀行按揭要求及重建樓宇結構。以下事項一般需要額外的家居、財物或責任保險。

傢俬及室內財物

梳化、床、電器、衣物、貴重物品 — 須由家居 / 財物保險承保。

漏水至樓下單位

對下層的漏水賠償責任屬家居保險範圍,火險不保。

盜竊及爆竊

失竊財物不屬火險保障,即使是火警期間發生亦然。

颱風 / 水浸(除非加保)

颱風、暴風、水浸及爆水管損失須額外加保延伸保障。

自然損耗及逐漸損壞

水管老化、生鏽、慢性滲漏、發霉及原有結構問題均不受保。

戰爭、核子及違法行為

標準保單不保戰爭、恐怖活動、核子風險,以及因物業作違法用途引致的損失。

火險常見問題

Loading…