餐廳 保險

專注美食,其餘交給我們 — 為中式、西式、咖啡、火鍋及外賣等餐飲業提供全面保障。

- 新客戶可享最高 9 折優惠

- 40+ 年中小企保險經驗

- 比較 30+ 家保險公司

- 1–2 個工作天內報價

上午遞交資料 — 即日簽發保險證書,準時滿足合約、場地或牌照要求。

我們承保的餐廳類型

由街坊茶餐廳到多店概念 — 我們按廚房、店面及團隊規模度身訂造保障。

中菜、湯品、粥品、點心、雲吞餃子

拉麵、鐵板燒、壽司刺身、韓燒

蛋糕、朱古力、中式糖水、西式糕點

茶餐廳、冰室、車仔麵、小食店

三文治、漢堡、Food Court

台式飲品、咖啡店、樓上 cafe、茶館

西班牙菜、法國菜、瑞士菜、葡國菜

火鍋、扒房、串燒、薄餅、素食

為您的餐廳提供全面保障

按需要組合保障模組 — 我們會根據菜式、店面及人手度身訂造條款、保額及自負額。

火險及財物全險

保障裝修、固定裝置、廚房設備及存貨因火災、水浸、盜竊或意外損毀的損失。

公眾/第三者責任

顧客跌傷、食物相關事故或財物損毀的索償,包括法律費用及和解金。

僱員補償保險

侍應、廚師、廚房及外賣員工的法定保障 — 工傷、職業病及身故。

營業中斷保險

因承保事故被迫停業時,補償毛利損失及持續經營開支。

金錢保險

保障店內、運送往來銀行途中及保險箱內現金,免受盜竊及搶劫損失。

團體醫療(可選)

員工住院、手術及門診保障 — 在餐飲業競爭激烈的勞動市場中吸引人才。

4 步輕鬆購買餐廳保險

提供基本資料

透過 WhatsApp 或查詢表格告訴我們餐廳類型、地址、營業時間、員工人數、職位及年薪。

正式報價

比較 30+ 家保險公司,1–2 個工作天內提供正式報價(大型或連鎖餐廳 3–4 天),列明保障範圍、不保事項及保費。

確認及提交文件

WhatsApp 確認後,提交已簽署的投保書、過往 3 個月強積金記錄及付款。

發出保單

收到付款後我們會通知保險公司發出電子保單(電郵/WhatsApp)或郵寄實體保單。

餐廳保險報價所需資料

請提供以下資料,我們通常可即日回覆報價。

- 投保人名稱 + 行業性質(西餐、茶樓等)

- 營業時間、地址

- 員工工種、人數、全年人工

- 店鋪面積、座位數目

- 店鋪裝修、貨物價值、機器價值

- 最近三年索償紀錄

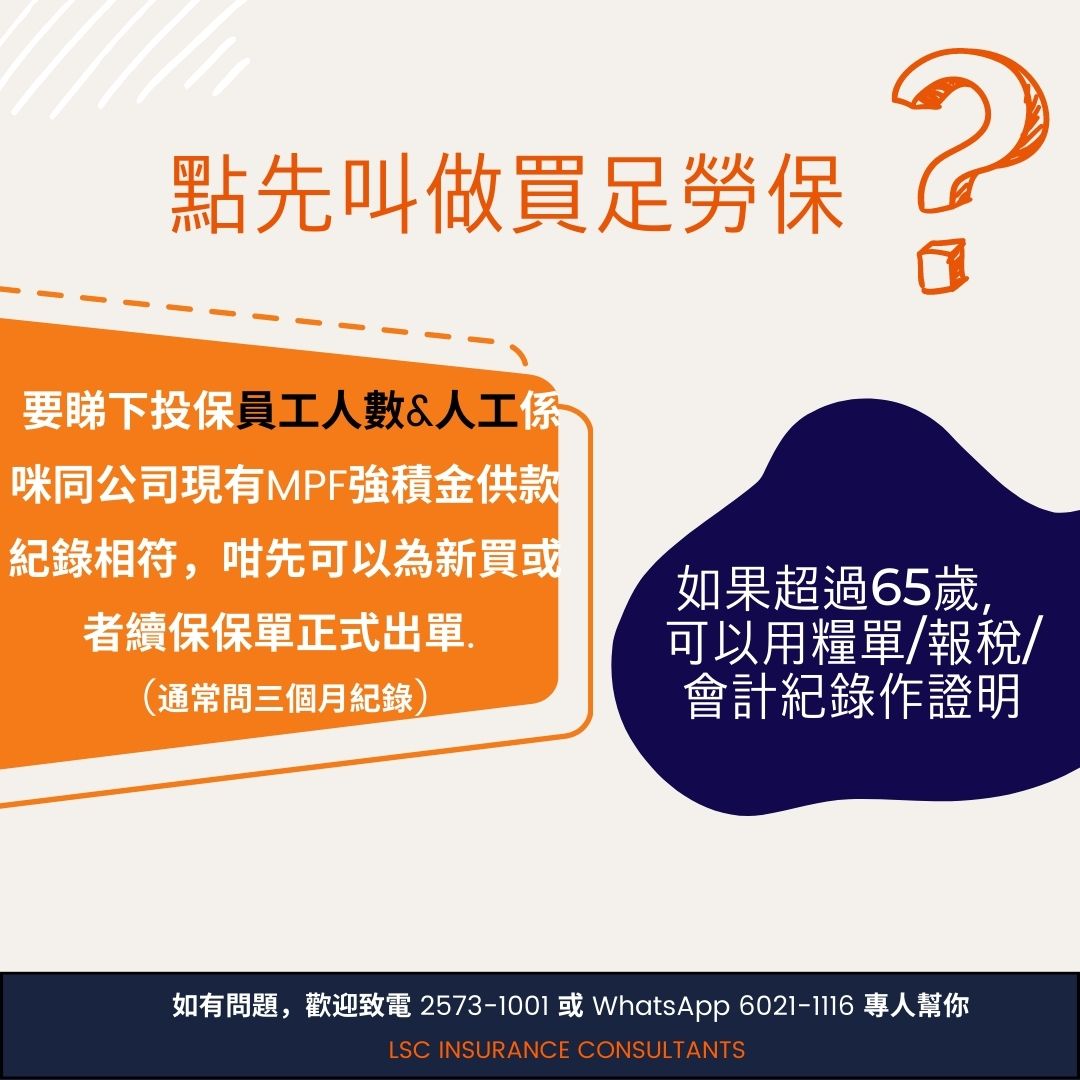

點先叫做買足勞保?

保險公司會核對投保員工人數及人工是否與公司MPF強積金供款紀錄相符;如有差異,索償時可能被打折甚至拒賠。以下是香港保險公司新買或續保時通常採用的準則。

人數及人工須與MPF紀錄相符

保險公司新買或續保前,通常會要求提交最近3個月的MPF強積金供款紀錄,核對員工名單、人數及人工是否一致。

65歲以上員工 — 可用其他文件證明

65歲以上員工豁免供強積金,可以用糧單、報稅表 (IR56) 或會計紀錄作為人工證明。

漏報/少報的風險

若索償時實際人工高於投保時申報,保險公司可按比例賠償(average condition),甚至以未如實申報為由拒賠。

- 申報總薪金(gross),而非實發薪金

- 包括花紅、佣金、津貼及加班費

- 增聘人手或加薪時要中途通知保險公司更新

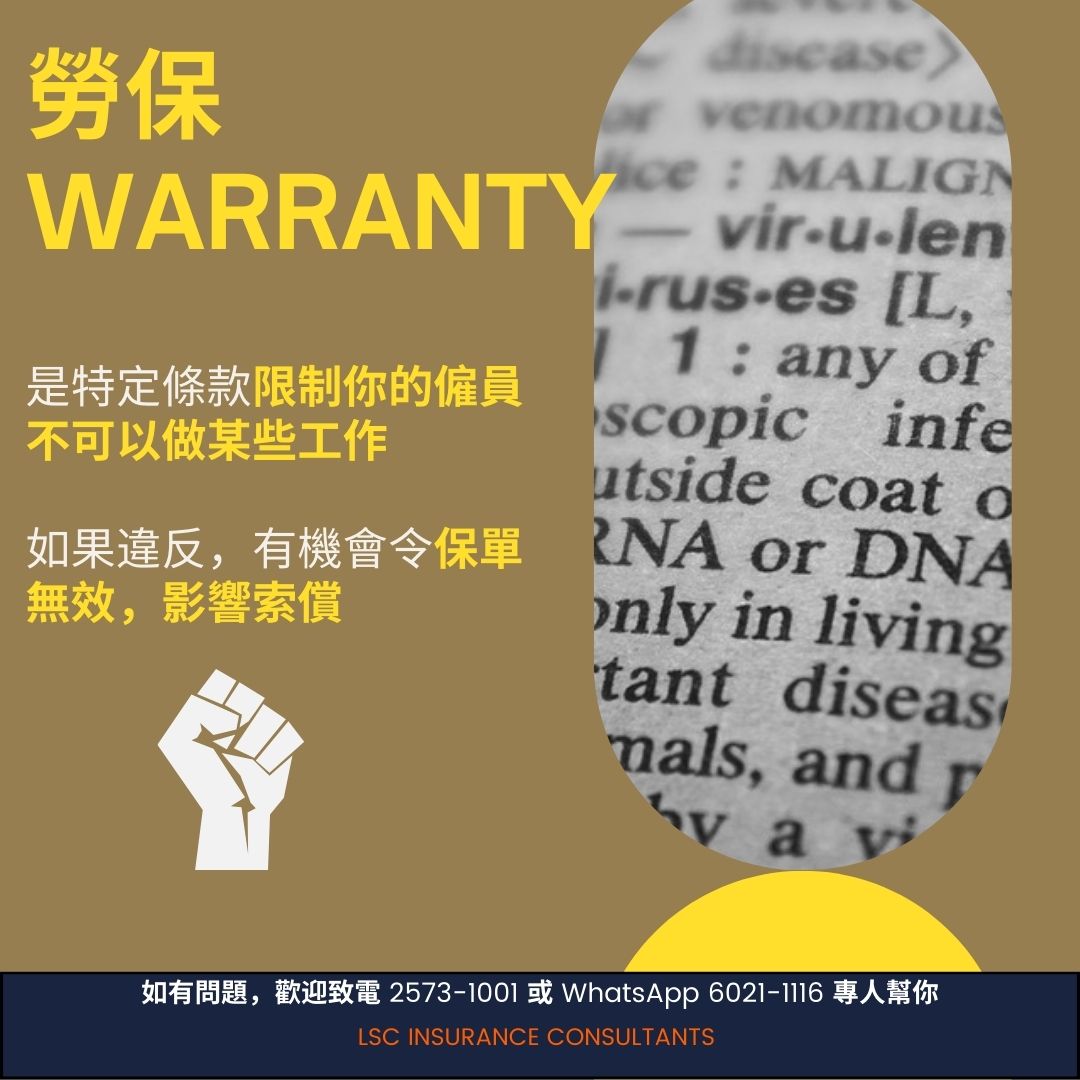

勞保 Warranty — 僱主必讀

保險公司通常會根據你的行業性質,在勞保保單上加入相關 Warranty 以控制風險。如果僱員實際工作違反 Warranty,有機會令保單無效,影響索償。

甚麼是 Warranty?

是特定條款,限制你的僱員不可以做某些工作。如果違反,有機會令保單無效,影響索償。

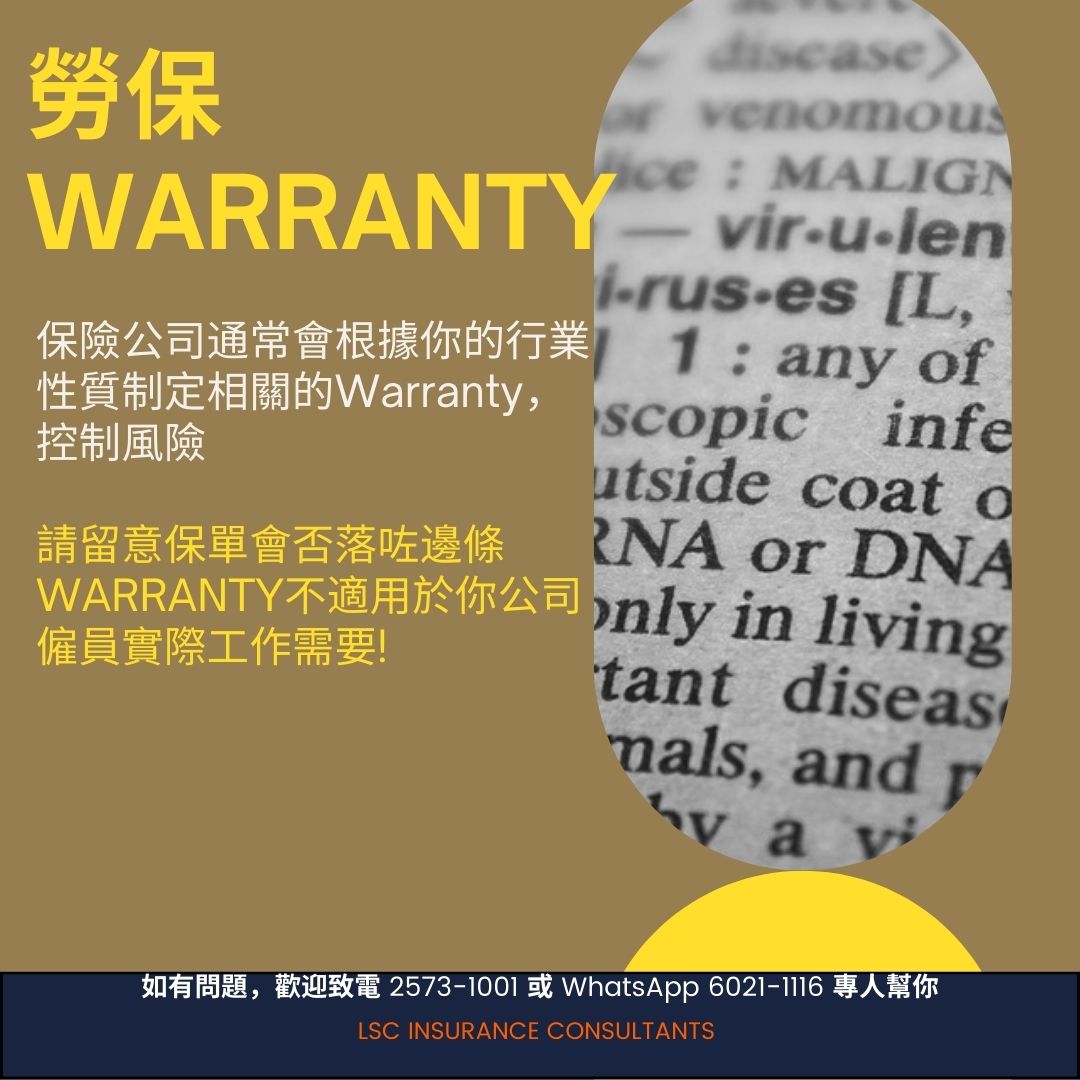

投保前必須核對

請留意保單會否落咗邊條 Warranty 不適用於你公司僱員實際工作需要。

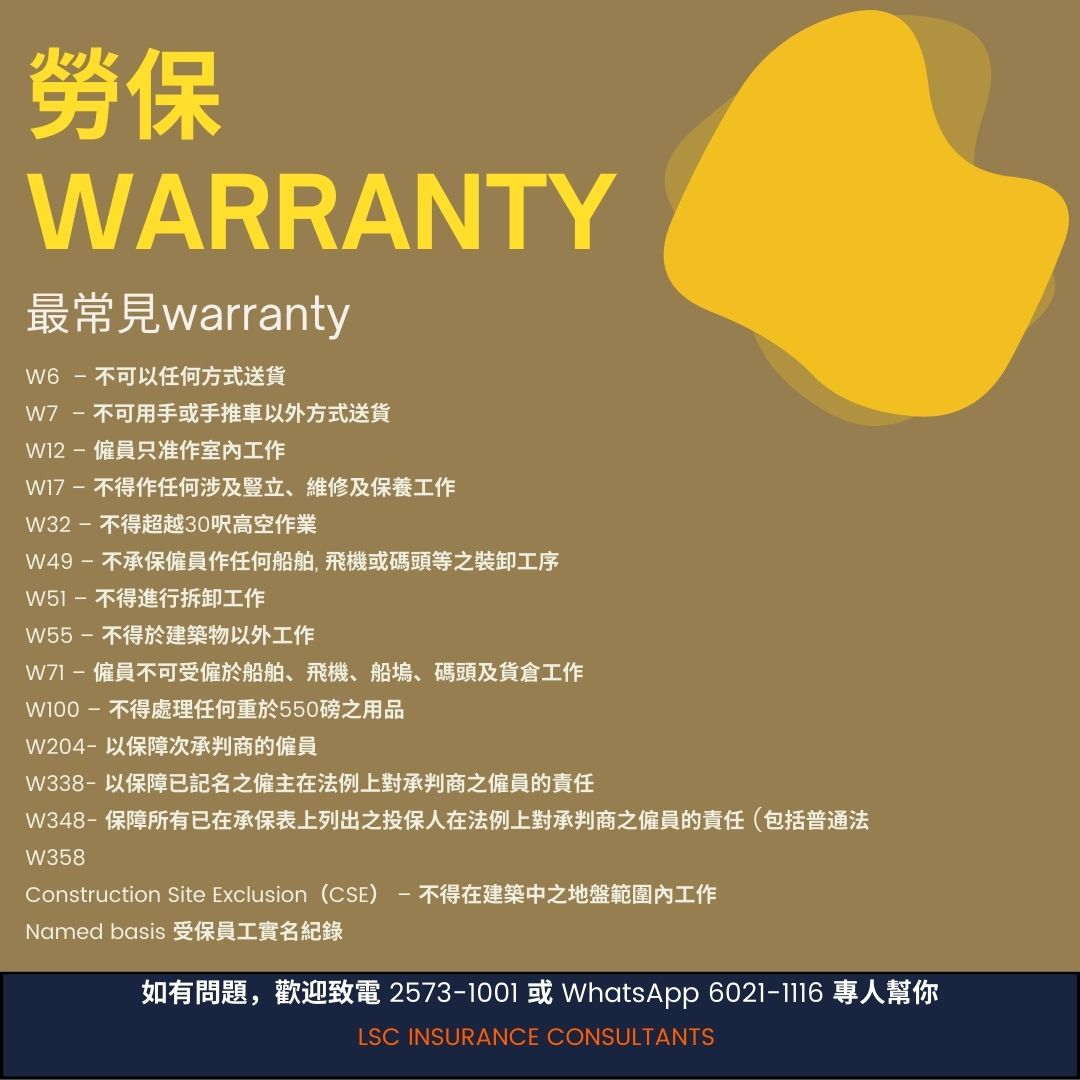

最常見勞保 Warranty

僅供參考,最終以保單為準。

- W6不可以任何方式送貨

- W7不可用手或手推車以外方式送貨

- W12僱員只准作室內工作

- W17不得作任何涉及豎立、維修及保養工作

- W32不得超越 30 呎高空作業

- W49不承保僱員作任何船舶、飛機或碼頭等之裝卸工序

- W51不得進行拆卸工作

- W55不得於建築物以外工作

- W71僱員不可受僱於船舶、飛機、船塢、碼頭及貨倉工作

- W100不得處理任何重於 550 磅之用品

- W204以保障次承判商的僱員

- W338以保障已記名之僱主在法例上對承判商之僱員的責任

- W348保障所有已在承保表上列出之投保人在法例上對承判商之僱員的責任(包括普通法)

- CSEConstruction Site Exclusion — 不得在建築中之地盤範圍內工作

- Named basis受保員工實名紀錄

不確定保單上的 Warranty 是否切合你的實際運作?將保單發給我們,我們會免費檢閱並標示有機會影響索償的條款。

邊啲角色需要計入勞保保障範圍?

根據《僱員補償條例》,只要存在僱主與僱員關係,無論工時、地點或合約性質均須投保。自僱人士及獨立外判工則不在保障範圍內。

需要受保

- 兼職僱員

- 受薪董事 / 老闆(有限公司)

- 海外受聘僱員

- 暑期工 / 實習生

- 兼職本地家務助理

不需受保

- 外判工(有自己僱員)

- 自僱人士(沒有僱主)

外判工應自行為其僱員購買勞保。

我係老闆,需唔需要買勞保?

答案視乎公司架構。重點:有限公司是獨立法人,即使老闆亦屬於公司「僱員」。

公司本身就是僱主。受薪董事/老闆與全體受薪員工皆屬公司僱員。

- 受薪董事 / 老闆 需要

- 受薪僱員 需要

老闆與公司在法律上是同一人,屬自僱人士而非僱員。只需為聘請的員工購買勞保。

- 老闆 = 自僱人士 不需要

- 受薪僱員 需要

已有保單?為何值得搵我們再報價

每年自動續保最容易畀貴錢,又或者買唔啱保障。花 5 分鐘攞個 alternative quote,至少可以拎到以下 3 個好處。

順便檢視現有保單

我們會幫你細閱現有保單,找出不再適用或保額不足的條款,避免理賠時先發現問題。

用「Clean Claim」攞更低報價

報價通常只睇過去 3 年賠償紀錄。如果舊意外已過 3 年,就當 clean claim 重新報價,往往可以幫公司慳到錢。

搵專做商業保險嘅顧問

如果現有代理主力做人壽/個人保險,未必熟悉勞保及商業理賠運作。專業商業保險顧問會全程跟進你的索償。